Wednesday, 22 February 2023

Fears a BHP slide could deliver -5% benchmark pullback; CEO hits US TV after earnings miss

by Berkeley Lovelace

BHP boss Mike Henry is manning the ramparts and rallying the dual-listed mining giant’s stakeholders following the company’s rare bummer of an earnings update.

Henry has been popping up on US broadcasters painting a rosy picture of BHP’s near-term outlook which he reckons is still full of promise.

With the share price trading more than 2% lower after its earnings report came in under expectations on Tuesday morning in Sydney, Henry told CNBC ahead of the US trading day that BHP’s (ASX:BHP) outlook remains strong, regardless of the steep drop in half-year profits.

Henry told CNBC that BHP still reckons the long-term outlook for commodities “remains strong,” buoyed by population growth, rising living standards and the metals demand accompanying energy transition, which includes steel-making raw materials.

But the real cause for optimism this year is the twin drivers of commodity demand in China and India, whose expected growth will spark resurgent demand for the key commodities that BHP produces – from copper through to iron ore and coal.

“We believe that Chinese growth and Indian growth are going to provide a bit of a counterbalance and support overall growth over the next six to 12 months, and beyond,” the CEO said.

Henry’s comments follow half-year profits which came in at US$6.46 billion, almost a full-third lower than the US$9.44 billion in the same period a year ago.

Tuesday’s 16% revenue slide for the six months into December has also turned a few heads, down from US$30.53 billion to US$25.71 billion.

BHP’s had a stupendous run as well, attributing the declines to lower iron ore and copper prices. During the six-month period, iron ore prices fell to a low of $80.03 per metric ton on Nov 1 while copper hit $3.29 a pound on Sept. 27.

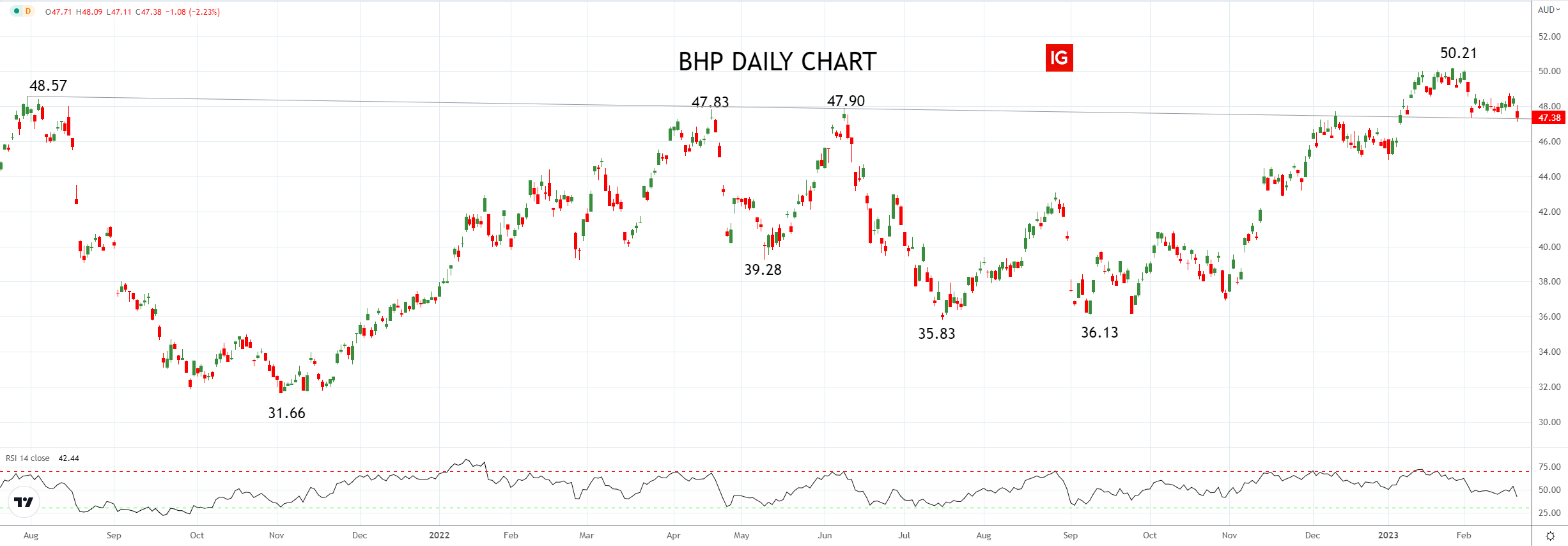

From a technical analysis POV of the BHP share price, IG’s Tony Sycamore says ASX200 traders are going to want the stock to hold the line.

“It’s imperative that the stock holds and closes above support coming from the horizontal trendline and breakout point at $47.30/20 to prevent a deeper pullback to $45.00.

This, Tony says, isn’t just about BHP.

The company is just such a monster that any sharp movement in the share price has significant implications at an index level.

“BHP accounts for an 11.1% weighting in the ASX200, so if BHP fails to hold support at $47.30/20, look for the ASX200 to take another leg lower towards 7200 in the coming session.”

Tony reckons such a breach is likely to be felt across the benchmark.

“That would give us the 5% pullback from the Feb 6. 7567 high we have been calling for since late January.”

Softening the blow for shareholders is the Board’s call to declare an interim dividend of 90 US cents per share (vs US88c expected), or about US$4.6 billion, which includes an additional amount of US$1.3 billion above the minimum payout policy.

That’s equivalent to a 69% payout ratio, 9% below last year’s HY21 payout ratio.

The post Fears a BHP slide could deliver -5% benchmark pullback; CEO hits US TV after earnings miss appeared first on Stockhead.